Premium holidays, childcare riders and health perks—decoding women-only term insurance

- October 29, 2025

- Posted by: Priya Sunder

- Categories: Financial Independence and women, Health Insurance, Livemint, Risk management

Insurance companies are experimenting with women-specific term plans, opening access to homemakers otherwise excluded for lack of income. Are they the right choice for women?

Written by Aprajita Sharma for Mint, 22 Oct 2025, with inputs from Priya Sunder, Co-founder, PeakAlpha

Term insurance offers the highest life cover at the lowest cost. However, despite its importance, penetration remains low as many people expect a maturity benefit from it. Eligibility is strict as well. One must have a steady income and be in good health to qualify.

In an attempt to broaden the appeal of term insurance, companies first opened it to homemakers, who were otherwise excluded for lack of income. Now, they are experimenting with women-specific term plans.

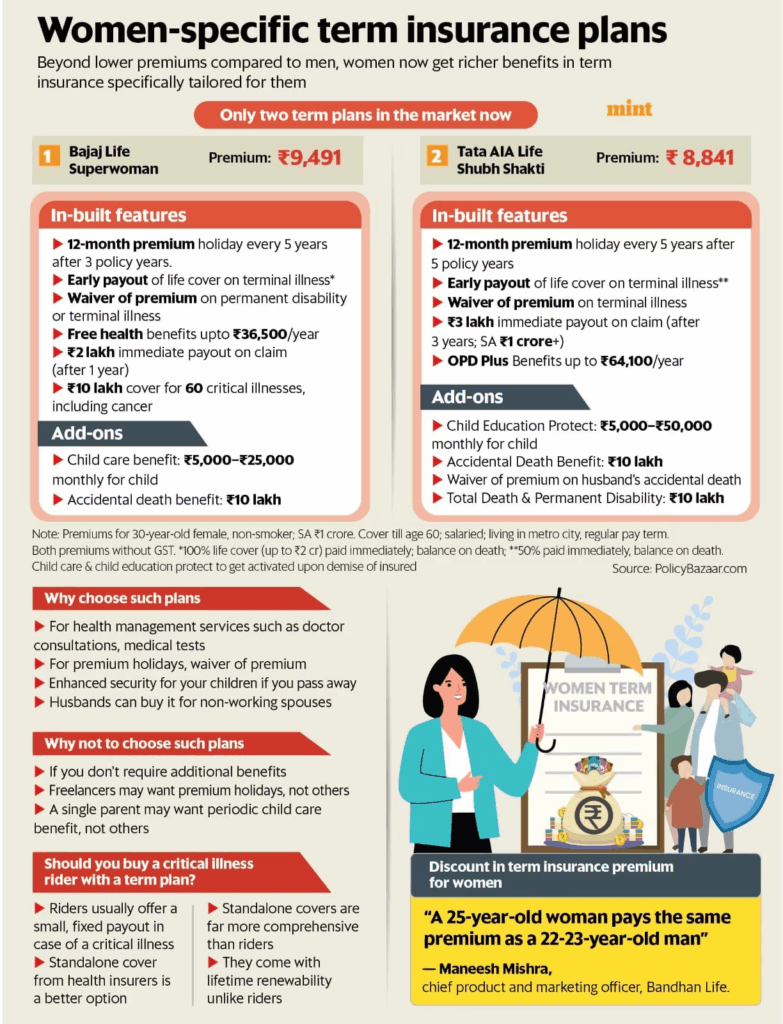

To broaden appeal, companies are now experimenting with women-specific term plans, opening access to homemakers otherwise excluded for lack of income. Only two such products exist currently—Bajaj Life Superwoman Term and Tata AIA Shubh Shakti.

“We have seen a sharp rise in women purchasing term plans. Today, one in five customers on our platform is a woman, up from one in 10 five years ago. This is driven by greater awareness and financial independence,” said Varun Agarwal, head of term insurance at Policybazaar.

Interestingly, women enjoy 5-10% lower premiums across insurers, but few are aware of this benefit. “They get an upfront discount because their mortality risk is lower than men’s. For instance, a 25-year-old woman pays the same premium as a 22-23-year-old man,” said Maneesh Mishra, chief product and marketing officer, Bandhan Life.

Women-specific term plans too come with this discount. The discount is automatic when you buy it as per your age and gender, without needing to be requested. “Some companies offer a three-year setback in age, others two. For us, it is three,” Mishra added.

Why do we even need women-specific term plans when the premiums are often comparable to regular term plans? Before we evaluate whether they’re worthwhile, let’s first take a look at what they actually offer.

Bajaj Life Superwoman Term

Bajaj Life became the first insurer to launch such a plan in March 2025. “The number of women customers has always been far lower than men in life insurance—especially in term cover—even though they enjoy lower premiums than men of the same age. The idea behind introducing a women-focused product was to offer richer features at the same price point,” said Madhu Burugupalli, head of product development and strategy, Bajaj Life.

The plan includes customer-friendly options such as a premium holiday of up to 12 months after a gap of every five years (once you complete three policy years) for those taking a career break or unable to pay premiums, waiver of premiums on permanent disability or terminal illness, free health services worth up to ₹36,500 annually (including health check-ups, maternity-linked support, in-clinic consultations with gynecologists, obstetricians, pediatricians, dermatologists, nutritionists and general practitioners), a ₹10 lakh cover for 60 critical illnesses including breast, ovarian and cervical cancers, and a ₹2 lakh immediate payout to nominees before full claim settlement.

An optional Child Care Benefit offers a steady monthly income to support a child’s education and living costs if the policyholder passes away. Monthly income will typically range from ₹5,000 to ₹25,000 as per the sum assured of the rider and be given until the child turns 25.

“While standard critical illness riders also cover women-specific conditions, what sets Superwoman apart are its health management services, premium holiday feature, and childcare rider—benefits that regular term plans don’t provide,” Burugupalli added.

Tata AIA Shubh Shakti

Tata AIA launched its women-specific term plan Shubh Shakti a month ago. The product offers life cover along with health benefits such as annual check-ups, cancer and PCOS screenings, and doctor consultations. It also allows a 12-month premium holiday after every five years (once you complete five policy years) on pregnancy or other grounds, provides an early payout on terminal illness, waives premiums on terminal illness, extends an immediate payout of ₹3 lakh on death, and includes OPD Plus benefits worth up to ₹64,100 annually.

The plan comes with a lifetime premium discount for single mothers, helping them maintain protection alongside essential responsibilities. Further, if the policyholder’s spouse dies in an accident, the insurer waives future premiums so that coverage continues uninterrupted.

While in-built OPD benefits cover annual full-body health checks, women-specific screenings, and consultations with specialist doctors (via telemedicine or physical visits), policyholders can opt for the Health Buddy Enhance rider to access additional wellness services such as teleconsultations, vaccinations, extra check-ups, and medicine discounts.

This plan too comes with a child education protection rider, in which monthly income ranges from ₹5,000 to ₹50,000 until the child turns 25.

Should you prefer such plans?

You need a cost-benefit analysis. Agarwal of Policybazaar says that women-specific health management services can translate into at least ₹5,000–6,000 of additional annual value, depending on how many benefits are actually used. “Such advantages are not available in regular term plans,” he noted. He added that two out of three women on Policybazaar’s platform now prefer women-specific term plans.

However, the real value lies in benefits that one actually requires. “Term plans offer protection against untimely death. Over time, many add-on benefits have emerged, such as payouts in case of accidents or disabilities. Women-specific term plans follow the same principle, but include features tailored for women, such as OPD benefits and premium holidays. The key is to see if you’ll actually use them—different strokes for different folks,” said Priya Sunder, co-founder and director at PeakAlpha Investments.

“Some women with sporadic income may value a premium holiday, while others may not need it at all. A single mother, for example, may find child care benefits useful, where payouts are given in chunks. If you do not plan to have children, such features may be irrelevant. The moment you add extra features and make the plan expensive, it loses the basic purpose of a term plan,” she added.

Suresh Sadagopan, founder of Ladder7 Wealth Planners, a fee-only financial planning firm, suggests such plans are still beneficial for working women, but homemakers should think twice. “Homemakers contribute significantly to the family with their unpaid work, but in terms of insurance, families need to consider how much premium they can afford across different covers while still having enough for expenses and investments. Logically, it makes sense, but practically, we have seen it does not always work out,” he said.

You need a cost-benefit analysis. Agarwal of Policybazaar says that women-specific health management services can translate into at least ₹5,000–6,000 of additional annual value, depending on how many benefits are actually used. “Such advantages are not available in regular term plans,” he noted. He added that two out of three women on Policybazaar’s platform now prefer women-specific term plans.

However, the real value lies in benefits that one actually requires. “Term plans offer protection against untimely death. Over time, many add-on benefits have emerged, such as payouts in case of accidents or disabilities. Women-specific term plans follow the same principle, but include features tailored for women, such as OPD benefits and premium holidays. The key is to see if you’ll actually use them—different strokes for different folks,” said Priya Sunder, co-founder and director at PeakAlpha Investments.

“Some women with sporadic income may value a premium holiday, while others may not need it at all. A single mother, for example, may find child care benefits useful, where payouts are given in chunks. If you do not plan to have children, such features may be irrelevant. The moment you add extra features and make the plan expensive, it loses the basic purpose of a term plan,” she added.

Suresh Sadagopan, founder of Ladder7 Wealth Planners, a fee-only financial planning firm, suggests such plans are still beneficial for working women, but homemakers should think twice. “Homemakers contribute significantly to the family with their unpaid work, but in terms of insurance, families need to consider how much premium they can afford across different covers while still having enough for expenses and investments. Logically, it makes sense, but practically, we have seen it does not always work out,” he said.