It doesn’t always pay to bank on fixed deposit

- November 27, 2020

- Posted by: Priya Sunder

- Categories: Financial planning, Fundamentals of Investing, Livemint, Risk management

- If most of their money is invested in fixed-income securities such as bank deposits and bonds, over time, the returns on these will struggle to beat inflation as rates fall

- The periodic increase and decrease in interest rates is a key monetary policy measure

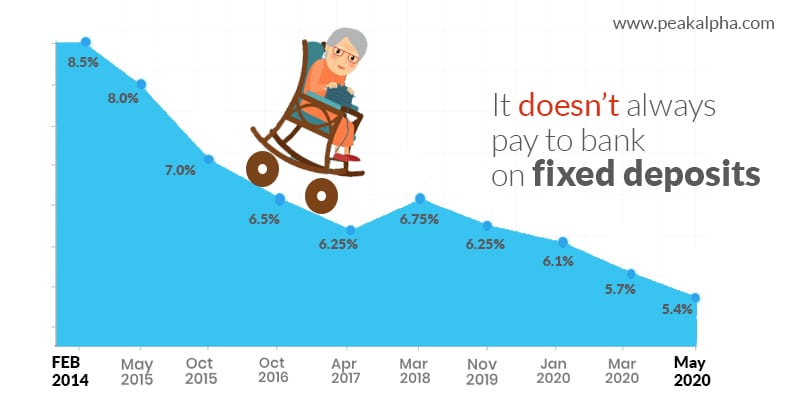

My 70-year old aunt is anguished every time the Reserve Bank of India (RBI) announces a rate cut. “I used to get 14% interest on my fixed deposits (FDs) at one time, and now I barely get 7%.” It is a common lament among retirees whose income ebbs with a fall in interest rates.

If most of their money is invested in fixed-income securities such as bank deposits and bonds, over time, the returns on these will struggle to beat inflation as rates fall. Retirees depend on the returns from a fixed corpus to fund expenses. If interest rates fall, they increase the draw-down from the corpus to meet expenses. If the draw-down rate is high, they run the risk of exhausting assets before their lifetimes. Alternately, to stretch their corpus, they reduce expenses, which can affect their quality of life.

The periodic increase and decrease in interest rates is a key monetary policy measure. Typically, interest rates are increased to curtail inflation and vice-versa. The current low rates are a measure to encourage borrowing, spur business growth and increase consumer spending. However, sustained low interest rates hurt retirees the most, since their capacity to earn fresh income is limited. Low returns on fixed-income instruments is akin to a pay cut for senior citizens.

As our economy develops, we will see more rate cuts. Many European countries have negative rates and several developed countries are at sub-3% rates. But one must also keep in mind that even though interest rates will continue to fall in the future, so will inflation. The high inflation rates seen in the past are unlikely to play out in the future. Hence, the real return on our investment (the difference between nominal return and inflation) may not be affected to the extent of the fall in interest rates.

Here’s how to make the best of a low-interest environment.

If you are a business owner, you may consider increasing your borrowing since loans will now come cheaper. You can even ladder your loans by borrowing at the current low levels to pay off older, higher-interest loans. As a retail investor, you can avail cheap property, car or personal loans. You can also refinance existing, expensive loans to cheaper ones.

Invest in alternate assets such as gold. Gold, typically, does well when borrowing cost is low, money supply is high, the economic outlook is uncertain, and equity market is volatile. However, be wary of investing in gold when the prices are already inflated. Have systematic investment in gold across the year, so you catch the low prices along with the high. Having at least 10% allocation to gold helps manage portfolio volatility better.

It is important to allocate a part of your portfolio to equity to beat inflation and taxation over the years. However, increased equity exposure could make the portfolio volatile in the short term. High volatility may be palatable for someone young, who has higher risk-taking and income-generating ability, but could make an older, risk-averse person quite nervous. Working with an adviser will help determine an equity allocation that is consistent with your risk appetite and future cash flows. Even conservative organizations like the Employees’ Provident Fund Organisation are now allocating a part of their portfolio to equity to beat inflation and generate higher long-term returns.

Interest on FDs attract tax slabs, which can be steep if you are in the highest tax bracket. However, investing a part of your portfolio in safe, high credit-quality, short-term debt funds can offer better tax-adjusted returns. If you redeem after three years from debt funds, long-term capital gains set in, which are taxed at 20% after indexation. Short-term gains are taxed at marginal rate.

A rupee saved is a rupee earned. If you need to generate regular income, consider systematic withdrawal plans (SWPs) from debt funds, which are more tax-efficient than FDs. If you invested ₹10 lakh in a 7% FD, you’ll earn an interest of ₹70,000 on which you would pay tax of about ₹21,000 (assuming you were in the 30% tax slab). If you invested the same amount in a debt fund, which also grew at 7% and you withdrew ₹70,000 after a year, your capital gains may be less than ₹5,000, on which you will pay a tax of ₹1,500, for the same tax slab. This is because the withdrawal in a debt fund is a combination of the principal and the gains, which reduces your tax bill, as opposed to the entire gains.

“That Senior-citizen Welfare Plan you recommended has saved me a heap of money in taxes!” exclaimed my aunt, who had just filed her returns last week. I briefly considered correcting her abbreviation of SWP, but her understanding of it was spot on. I smiled and left it at that.